National Debt: The Inheritance

Part 1, The Problem: Decades of spending choices and the refusal to pay for them have produced a debt larger than the American economy. Someone will pay for it. Just not the people who ran it up.

U.S. government debt has been a fixture of American life for decades. And it hasn’t seemed to matter. Markets keep humming. The economy keeps growing. Life goes on.

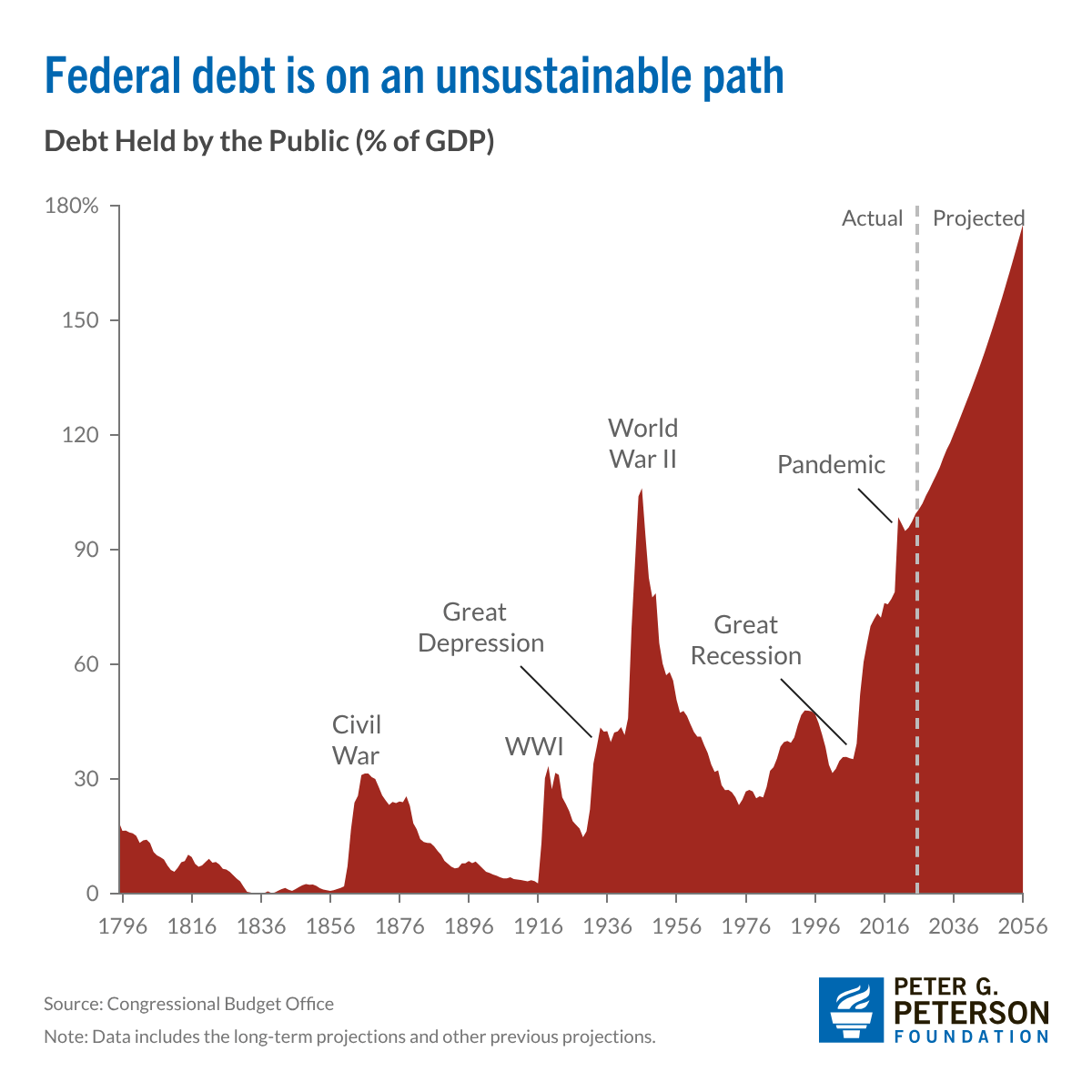

Yet, the national debt recently surpassed the size of the entire U.S. economy. The federal government is on its way to setting a new all-time record for indebtedness, and there is little end in sight. Now, some are sounding alarms they haven’t sounded before about the risks it presents today, and the burden it places on the next generation.

Today, we explore the problem and why it should matter. Next week: what’s driving this. The week after: what solutions might actually look like. Every Solving For series is available to read or listen to — I narrate each one myself —at solvingfor.io.

Robert Giaimo and Henry Bellmon had almost nothing in common.

Giaimo was the son of an Italian immigrant banker, raised in New Haven, Connecticut, educated at Fordham and the University of Connecticut law school, a Democrat who spent two decades in the House representing the factory workers and union households in southern Connecticut. Bellmon was born on a farm near Tonkawa, Oklahoma, the son of a Cherokee Strip pioneer, a man who worked his way through Oklahoma A&M College, saw battle as a first lieutenant at Saipan and Iwo Jima, and served two terms in the U.S. Senate, repeatedly returning to his wheat and cattle farm in Noble County. He was a Republican, but he considered himself, above all else, a farmer.

In 1980, both men left the U.S. Congress. They had spent years on opposite sides of the House and Senate Budget Committees — Giaimo as chairman in the House, Bellmon as the ranking Republican in the Senate — watching from the inside as the federal government found it consistently easier to spend than to choose. They had seen the oil shocks, the stagflation years, the beginning of what would become a structural mismatch between what the government promised its citizens and what it was willing to collect from them.

When they left, rather than simply returning to private life, they did something unusual: they decided the problem required an institution. On June 10, 1981, they joined together to incorporate the Committee for a Responsible Federal Budget — a nonpartisan organization devoted to the proposition that the country's fiscal path was unsustainable and that someone, outside the political pressures of government, needed to keep saying so.

Nearly 45 years later, the organization's president, Maya MacGuineas, explained how far the problem had traveled.

“It’s happened,” she declared in April 2026. “The national debt is now larger than the U.S. economy, about twice the historic average. We’ve heard plenty of alarm bells in the past few years about our fiscal path, but this one rings especially loudly.”

The Congressional Budget Office projects that by the end of the decade the U.S. will set a new all-time record for debt held by the public — surpassing the 106 percent of gross domestic product reached in the immediate aftermath of World War II.

Unlike that debt, which the country reduced systematically over the following three decades, this one has no equivalent plan behind it — just a projection that keeps climbing. And there is a big difference, MacGuineas noted, between that moment and this one. The post-World War II debt was the price of defeating fascism. This one, she said, is the result of “a total bipartisan abdication of making hard choices.”

Why It Matters

This three-part Solving For series explores America’s national debt: why it matters, the forces that got us here, and what a way forward could look like.

It's a problem that has long escaped serious attention or any meaningful reform. But the consequences are no longer theoretical. Continued inaction carries risks to the economy, to American competitiveness, and to a generation that will inherit the bill without having agreed to run it up.

The interest payments on the debt are now the federal government's second largest spending category — more than national defense or Medicare, trailing only Social Security. Within a generation it's projected to become the federal government's single biggest expense, crowding out every public investment that historically drives prosperity: education, infrastructure, research, healthcare.

Today, nearly one-fourth of those interest payments flow to foreign countries, including China, “to build their economies rather than our own,” according to RAND, one of the country’s most respected national security and policy research institutions.

Meanwhile, the debt makes borrowing more expensive for every American who needs a mortgage, a car loan, or a business line of credit. The reason: government borrowing at this scale competes with every other borrower in the same capital markets — and it always wins, driving up the cost of credit across the entire economy.

It shrinks the fiscal space available to respond to the next crisis. 2008 brought a Great Recession; 2020 brought COVID-19 and a global pandemic. There will be another.

It puts Social Security and Medicare on an insolvency countdown that, without action, ends in automatic benefit cuts for those who need them most.

At a time when the gap between the wealthiest Americans and everyone else has reached the widest point in decades, it dramatically limits the government's capacity to find solutions.

And it carries the risk of a sudden loss of market confidence that turns an outsized debt burden into a full-blown financial crisis.

It’s so concerning that — despite structural advantages like the U.S. dollar's reserve currency status, the depth of American capital markets, and the scale of the U.S. economy — Hank Paulson, former Treasury Secretary under George W. Bush, warned in April: “We need an emergency break-the-glass plan…so it’s ready to go when we hit the wall.”

When. Not if. And when it comes, he said, “It will be vicious.”

But the deepest problem isn't the number. A government that spends more on interest payments for past decisions than investments in future growth is one that has stopped making choices — and started living with the consequences of decisions it can no longer take back.

The World’s Richest Debtor

To understand the problem of America’s national debt, start with the economy itself.

The United States has the largest economy in the world — by far. As of the close of the first quarter of 2026, American GDP stood at $31.22 trillion — more than one quarter of all global economic output. For context: China is second at $19.4 trillion, Germany a distant third at just over $5 trillion, and Japan fourth at $4.28 trillion. The U.S. has been the most productive economic engine in human history for more than a century.

And yet. As of March 31 of this year, federal debt held by the public stood at $31.27 trillion — larger than the largest economy in the world. That figure refers to what the government owes outside investors, as distinct from the gross debt figure of $39 trillion, which includes money the government owes to itself.

The debt grows because the federal government continues to run large annual budget deficits — the yawning gap between what it collects in revenue and what it spends each year. To cover the difference, the government borrows by issuing Treasury bonds, compounding the debt.

Consider 2025. The federal government collected $5.2 trillion in revenue and spent $7.0 trillion. The $1.8 trillion gap was borrowed and added to the debt.

It's an especially alarming case of financial mismanagement, but not an anomaly. With a few exceptions, it's become the operating condition of the United States government, sustained across administrations and Congresses of both parties for decades.

The deficit is a two-sided problem. The spending side gets most of the attention. The revenue side is equally revealing — and equally the result of deliberate choices made over decades. Part Two will examine those choices, including a consequential and long-running debate about how investment income is taxed compared to wages — particularly for the wealthiest Americans.

The 2025 budget illustrates the basic picture: where the money comes from, and where it goes.

Of $5.2 trillion in tax revenues, just over half came from individual income taxes on both wages and investment gains — two forms of income the tax code treats very differently; roughly one-third from payroll taxes that fund Social Security and Medicare; about seven percent from corporate income taxes; and the rest from a mix of excise taxes, tariffs, and fees.

The $7 trillion in federal spending falls into three categories, and the proportions reveal something important about the country's actual priorities — not as stated, but as enacted.

The first and largest is mandatory spending: programs governed by permanent law that run on autopilot unless Congress specifically acts to change them. Mandatory outlays totaled $4.2 trillion in 2025 — more than half of the entire federal budget. Social Security, the retirement and disability program, costs roughly $1.6 trillion a year. Medicare — the federal health insurance program for Americans 65 and older — accounts for nearly $1 trillion, and Medicaid — health insurance for low-income Americans of all ages — another $670 billion. These are not discretionary line items subject to annual negotiation. They are legal promises made to tens of millions of Americans who have spent their working lives paying into the system.

The remaining roughly $900 billion in mandatory spending funds other legally mandated commitments: veterans' benefits, federal employee retirement, student loan programs, and agricultural subsidies.

The second is discretionary spending — programs Congress funds through annual appropriations, subject to yearly negotiation. In 2025, discretionary spending was just 27 percent of the total budget. Defense accounts for the largest share of that — roughly $900 billion. The Trump administration is seeking to increase that figure to $1.5 trillion in the coming fiscal year. Everything else that most people associate with the federal government — education, transportation, scientific research, environmental protection, housing, foreign aid — competes for what remains.

When politicians talk about cutting government spending without touching entitlements or defense, they are negotiating over a relatively small fraction of the whole.

The third is interest on the national debt. In 2025, that totaled nearly $1 trillion — $2.8 billion every day. Interest has become the fastest-growing line item in the entire federal budget. No roads, no research, no benefits, no security. It is the pure cost of decisions already made, extracted from the present.

Stated plainly, the federal budget reflects a specific set of national priorities that have been locked in across decades of legislation: supporting the retirement income of older Americans, funding healthcare for the elderly and the poorest Americans, maintaining a global military presence, and increasingly, servicing the debt accumulated while pursuing all three. Everything else — the investments that tend to determine a country’s future — is funded from what remains after those obligations are met.

In 2025, that remainder was not enough to cover the obligations themselves.

The Generation That Didn’t Vote for This

Researchers at the Harvard Kennedy School conduct what many consider the gold standard of American youth polling — a nationally representative survey of young adults ages 18 to 29, now in its 51st edition. The findings released in December 2025 told an unambiguous story. More than four in ten young Americans said they were struggling or getting by with only limited financial security. A clear majority said the country was on the wrong track. Money was at the root: the sense that the economic system their parents described to them is not the one they actually inherited.

Behind that instability is a specific and measurable inheritance. The generation now entering its working years is the first to do so inheriting a national debt larger than the entire economy — accumulated across decades of decisions made entirely by others. They did not vote for the tax cuts. They did not vote for the unfunded wars. They did not vote for the entitlement expansions or the emergency stimulus programs or the structural mismatch between what the government promised and what it was willing to collect. They are, in the precise sense, inheriting a bill they never agreed to run up.

The people bearing the consequences are not the people who made the decisions. That is not an accident. It is the natural outcome of a democratic system in which the costs of present decisions are deferred long enough that those who will pay them cannot yet vote.

Robert Giaimo and Henry Bellmon saw this coming in 1981. They built an institution to say so, and that institution has been saying so for nearly 45 years. The alarm has not changed. The distance between where it was first sounded and where we now stand has. The debt has crossed 100 percent of GDP. Interest payments have surpassed defense spending. A former Treasury Secretary is calling for an emergency break-the-glass plan. And a generation is entering a world shaped entirely by decisions made before they arrived, by leaders who will not be here to answer for them.

The bill, as bills sometimes do, has found its way to the last people left at the table.

Prefer to listen? I narrate each edition myself. Find the audio at the top of this page or under the Listen tab at solvingfor.io.

If this resonated, please give it a like and share with someone you think would enjoy it.

Solving For takes on one pressing problem at a time: what’s broken, what’s driving it, and what a path forward might look like.

Previous series have examined rare earth dominance, AI safety, the decline of local news, the end of amateurism in college sports, shrinking competition in Congress, social media and teen mental health, and a world rearming as the global rules-based order weakens. Learn more at solvingfor.io.