National Debt: The Abdication

Part 2, The Forces: The Bill That Keeps Getting Passed Forward — and Why It May Finally Matter.

In Part Two of our series on the national debt, we turn to the forces that built it. How a budget director's confession in 1981 revealed the mechanism that would define the next four decades. How Congress repeatedly lowered taxes on wealth while expanding what the government promised to spend. How 73 million Baby Boomers created a structural deficit no single Congress has been willing to fix. And how rising interest rates may finally be closing the window that allowed Washington to defer the reckoning.

Missed Part One? Go here to understand why the national debt — now larger than the entire U.S. economy — should matter to every American, and why the generation now entering the workforce is the first to inherit a bill they never agreed to run up. Part Three will explore solutions.

Prefer to listen? I narrate each edition myself — audio for this installment is coming soon. In the meantime, Substack's built-in audio is available. All series are at solvingfor.io.

In September 1789, Thomas Jefferson sat down in Paris to write James Madison a letter about money he believed no one had the right to spend.

The city around him was coming apart — the French Revolution only weeks old, the Bastille having fallen in July, the monarchy buckling under debts it could no longer service. Watching the living taxed for debts they had never chosen, Jefferson wrote Madison: “the earth belongs… to the living.” No generation should be able to bind the next with debt it cannot repay within its own lifetime — which Jefferson, working from mortality tables, set at about 19 years.

By 1803, Jefferson sat in Washington as the third president of the United States, and the question he'd put to Madison was about to land on his own desk. Napoleon’s France was willing to sell the Louisiana Territory, and the price was money the young government did not have.

Madison, the man Jefferson warned about the danger of binding future generations, was now his secretary of state. The two men who had argued on paper over whether one generation may mortgage the next found themselves, together, committing the republic to the largest debt of its short life.

The terms: about $15 million for 828,000 square miles, doubling the size of the country in a single stroke. But the U.S. government did not have the funds in its treasury, nor did America have the capital markets to raise it. The new world turned to the old, issuing bonds through two European banks: Baring & Company in London and Hope & Company in Amsterdam — debt that America would spend two decades repaying, the final installment in 1823. Even the bankers were uneasy. Sir Francis Baring wrote of trembling “at the magnitude of the American account.”

They did it anyway — the purchase encompassed 15 future states, the greatest real estate transaction in history.

The story captures two strands of America's relationship with debt — wary of it in principle, willing to shoulder it when the stakes demanded it.

The Louisiana Purchase was not an exception. America had been born in debt following the Revolutionary War — the first U.S. treasury secretary, Alexander Hamilton, argued that a manageable debt was a national blessing: committing creditors to the new government's success and building the credit the country would need.

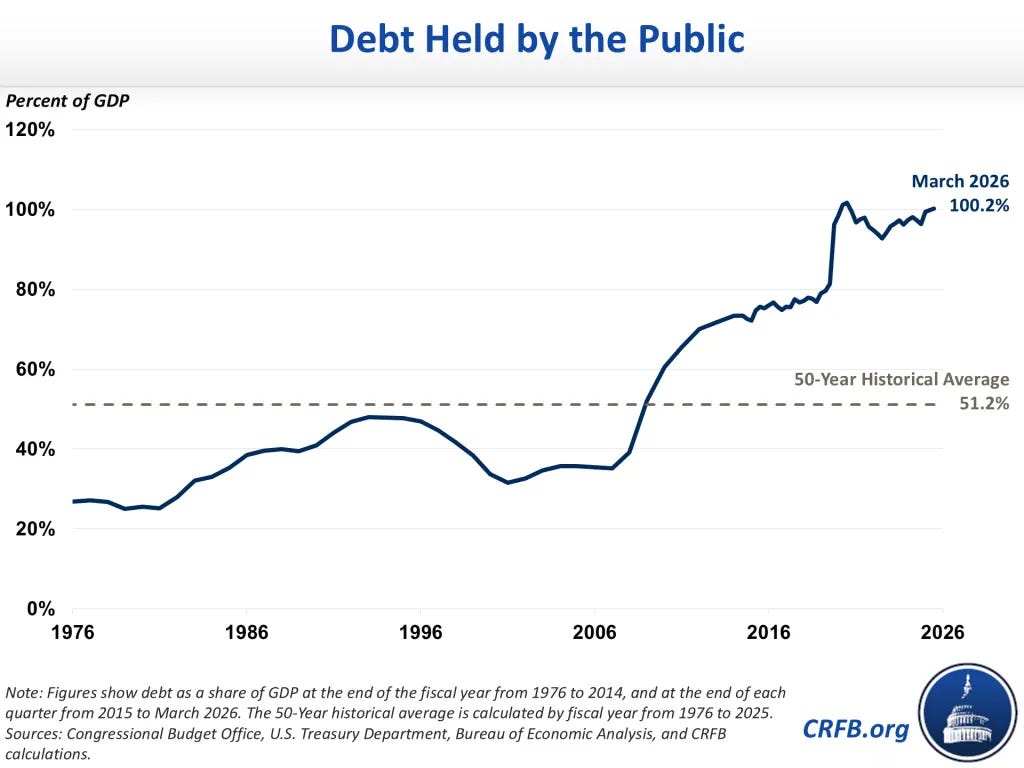

Through its history, the country borrowed a great deal — to survive the War of 1812, to preserve the Union through the Civil War, to lift itself out of the Great Depression, and to fight two world wars. World War II pushed federal debt to a record 106 percent of GDP in 1946 — and over the next three decades, the country paid it down to roughly a quarter.

The borrowing had a beginning, a reason, and an end.

Today, that’s no longer the case.

The country is now adding debt at a rate that will eclipse the post-World War II record by the end of the decade, with no end in sight. But there is no war to point to. No depression to climb out of. No continent to acquire. The federal government keeps borrowing without the discipline that once restrained it, or the purpose that justified it.

Deficits Don’t Matter

Today’s debt problem stems from three choices, repeated over the past 45 years until they hardened into habit.

First, politicians committed to things they were unwilling to ask voters to pay for — tax cuts, wars, new benefits. Rather than raise taxes or cut spending, they let borrowing close the gap, knowing voters rarely held them accountable for the deferral. The bill would come later, after they’re gone.

Second, the tax burden increasingly shifted away from wealth and toward work, asking more of the paycheck than the investment portfolio. The shift reduced federal revenues and added to the debt.

Third, Americans lived longer, and the cost of supporting an aging population through programs like Social Security and Medicare continued to climb. What had once been manageable obligations became steadily larger claims on the federal budget.

The roots of the modern era of debt politics can be traced to 1981.

David Stockman, Ronald Reagan’s 35-year-old budget director, spent much of that year arguing that cutting taxes while increasing defense spending would actually shrink the deficit.

Then, in a series of conversations with journalist William Greider that became a damaging profile in The Atlantic that December, he admitted the numbers didn’t add up. Future spending cuts had been replaced by what he called the “magic asterisk”: promises of savings that had never been specified.

The tax cuts were signed. The spending cuts largely were not.

The deficit the asterisk concealed did not disappear. It was simply handed forward.

The details would change. The incentives would not.

There was a brief interruption in the late 1990s, when President Bill Clinton, a Democrat, and a Republican-controlled Congress produced balanced budgets and reduced the debt.

Then the pattern returned.

The 2001 and 2003 tax cuts under President George W. Bush erased projected surpluses. The Afghanistan and Iraq wars were financed through borrowing but, unlike previous wars, without higher taxes or war bonds. America had borrowed to fight wars before. What was new was fighting them while cutting taxes, leaving the bill for future taxpayers. In 2003, Congress added a Medicare prescription drug benefit without identifying how to pay for it.

Former Treasury Secretary Paul O’Neill later recalled that Vice President Dick Cheney dismissed deficit concerns with a simple conclusion from the Reagan years: “deficits don’t matter.”

Borrowing was no longer an exception. It was becoming standard operating procedure.

Then came two genuine emergencies: the financial crisis and the pandemic. Both required massive federal intervention. Both also left the government with a permanently higher fiscal baseline.

Most of the Bush tax cuts were made permanent in 2012 under President Barack Obama, with bipartisan support in Congress. The 2017 Tax Cuts and Jobs Act signed by President Donald Trump cut individual taxes again without offsets and reduced the corporate rate from 35 to 21 percent — the largest such cut in U.S. history. In 2025, Trump and a Republican-controlled Congress extended many of those cuts through the "One Big Beautiful Bill," which the Congressional Budget Office estimated would add $3.4 trillion to the deficit over the next decade.

Debt ceased to be an emergency measure reserved for wars, recessions, or national projects. It became the routine way Washington avoided hard choices.

In 2010, Stockman, a Republican, wrote that the seeds had been planted in 1981, lamenting the “Republican Party's embrace, about three decades ago, of the insidious doctrine that deficits don't matter if they result from tax cuts.”

Taxing Work, Rewarding Wealth

The second shift was quieter than the rise of deficit politics, but just as consequential.

In a 2011 op-ed, titled “Stop Coddling the Super-Rich,” Warren Buffett disclosed that he had paid a federal tax rate of 17.4 percent the previous year. His secretary, Debbie Bosanek, had paid 35.8 percent. The difference was not that Buffett concealed income. It was that most of his earnings came through capital gains and dividends — taxed at lower rates than wages. She was paying more than twice his rate. It was entirely legal.

But the Buffett-Bosanek contrast was not an anomaly. It was the system working as designed.

Over the last 45 years, Congress repeatedly lowered taxes on investment income relative to wages, arguing that lower taxes on capital would encourage entrepreneurship, investment, and economic growth. Today, the top federal tax rate on ordinary income is 37 percent, while long-term capital gains are generally taxed at 20 percent.

The shift changed who carried the tax burden. Wages are taxed automatically through payroll withholding. Investment gains can accumulate for years before being taxed and, when realized, often face lower rates. As asset values rose, more income flowed through forms taxed more lightly than labor.

The full scale of the divide came into view in 2021, when ProPublica published leaked IRS data showing that some of America's wealthiest individuals — including Jeff Bezos, Elon Musk, and Michael Bloomberg — had paid little or no federal income tax in certain years, their wealth surging while taxable income remained small.

The question is simple: why was the government repeatedly lowering taxes on wealth while its commitments — and its debts — kept growing?

The result was not that the wealthy paid no taxes. Many paid enormous sums. The result was that the tax base increasingly leaned on earned income while much of the country’s fastest-growing wealth received preferential treatment.

The government had committed itself to large and growing obligations while simultaneously pulling back from taxing some of the fastest-growing sources of wealth. The gap, once again, was filled with borrowing.

No One Voted for This

The third force is different in character from the first two.

Politicians chose to borrow rather than tax or cut. Politicians chose to tax investment returns more lightly than work. But no politician chose to make Americans older. No one decided that Baby Boomers would retire in waves, that lifespans would lengthen, or that healthcare costs would rise faster than the economy. These things simply happened — and the government’s finances were not built to absorb them.

That was David Walker’s message, and he delivered it to anyone who would listen.

Walker served as U.S. Comptroller General from 1998 to 2008 — the country's chief auditor — and became one of Washington's most persistent voices warning that the long-term fiscal trajectory was worse than most Americans understood.

He took his case on the road in the “Fiscal Wake-Up Tour,” and his warnings became the subject of a 2008 documentary, I.O.U.S.A. Few in Washington were listening.

That was 17 years ago. The debt has since grown fivefold.

The programs at the center of Walker’s alarm — Social Security and Medicare — were designed for a different America. When Medicare was established in 1965, there were roughly four workers for every retiree. The math worked because the young were numerous and the old were not.

That ratio has been narrowing ever since. The Baby Boom generation — 73 million Americans born between 1946 and 1964 — began retiring around 2010 and will continue through the mid-2030s. Lifespans have lengthened. Birthrates have fallen. By 2035, there will be roughly 2.4 workers supporting each Social Security beneficiary, down from four a generation ago.

Healthcare compounds the problem. Medicare costs do not just grow with the number of retirees; they grow with the cost of care itself, which has consistently outpaced inflation and economic growth. An aging population consumes more healthcare, and that healthcare becomes more expensive every year.

The result is a structural deficit that no one voted for and no single Congress created. Social Security and Medicare face a combined funding shortfall of nearly $78 trillion over the next 75 years, according to the programs' trustee reports. The Social Security trust fund is projected to be exhausted by 2033 — seven years from now — at which point benefits would be automatically reduced unless Congress acts. These are not speculative scenarios. They are the official projections of the programs’ own trustees.

This force, unlike the first two, requires no bad faith to explain. The politicians who built these programs were not concealing a time bomb. They were designing a safety net for their moment.

The country changed. The programs largely have not.

This Time May Be Different

Three forces brought the United States to this point: decades of borrowing to avoid difficult choices, a tax system that increasingly favored investment over work, and demographic changes that steadily increased the cost of programs like Social Security and Medicare.

For years, the consequences seemed manageable. The debt grew, but so did the economy. Growth often outran the government’s borrowing costs, allowing Washington to carry ever-larger obligations without an immediate reckoning.

That advantage may be fading, and the reason is interest rates.

Economists have a shorthand for the relationship: r > g, where r is the government's borrowing rate and g is economic growth. When growth is faster than borrowing costs, debt is generally easier to manage. When borrowing costs exceed growth for sustained periods, debt becomes much harder to stabilize.

Interest rates have risen sharply from the ultra-low levels that prevailed for much of the 2010s. The Congressional Budget Office projects that within the next decade the government’s average borrowing costs could exceed the economy’s growth rate — a shift that would make the debt far more difficult to stabilize and increase the risk of a debt spiral.

That prospect has begun to change minds.

In a May 2026 essay for The Atlantic, economist Jared Bernstein noted that he had spent much of his career dismissing claims that a high debt-to-GDP ratio signaled imminent crisis. But if interest rates begin to outpace growth, he argued, the calculus changes. “If you’re not worried about this country’s fiscal outlook,” Bernstein wrote, “you’re not paying enough attention.”

Jefferson’s warning more than 230 years ago was about more than debt. It was about accountability — the idea that the people who make a decision should be the ones who live with it. For most of American history, that principle held, imperfectly but recognizably: wars were fought and paid for, crises met and resolved. What the past 45 years produced is something different — debt without emergency, spending without payment, commitments made by one generation and quietly handed to the next.

At some point, there is no one left to pass it to.

Prefer to listen? I narrate each edition myself. Find the audio at the top of this page or under the Listen tab at solvingfor.io.

If this resonated, please give it a like and share with someone you think would enjoy it.

Solving For takes on one pressing problem at a time: what’s broken, what’s driving it, and what a path forward might look like.

Previous series have examined rare earth dominance, AI safety, the decline of local news, the end of amateurism in college sports, shrinking competition in Congress, social media and teen mental health, and a world rearming as the global rules-based order weakens. Learn more at solvingfor.io.